For all merchants selling into Europe there are big changes are on their way from the 1 July 2021 to the way that VAT is charged and collected.

Changes going forward:

The key difference between taxes and duties is that duties are a type of tax on goods entering or leaving a country, while taxes are charges placed on almost all purchases. Both contribute to the total import and export costs of a product.

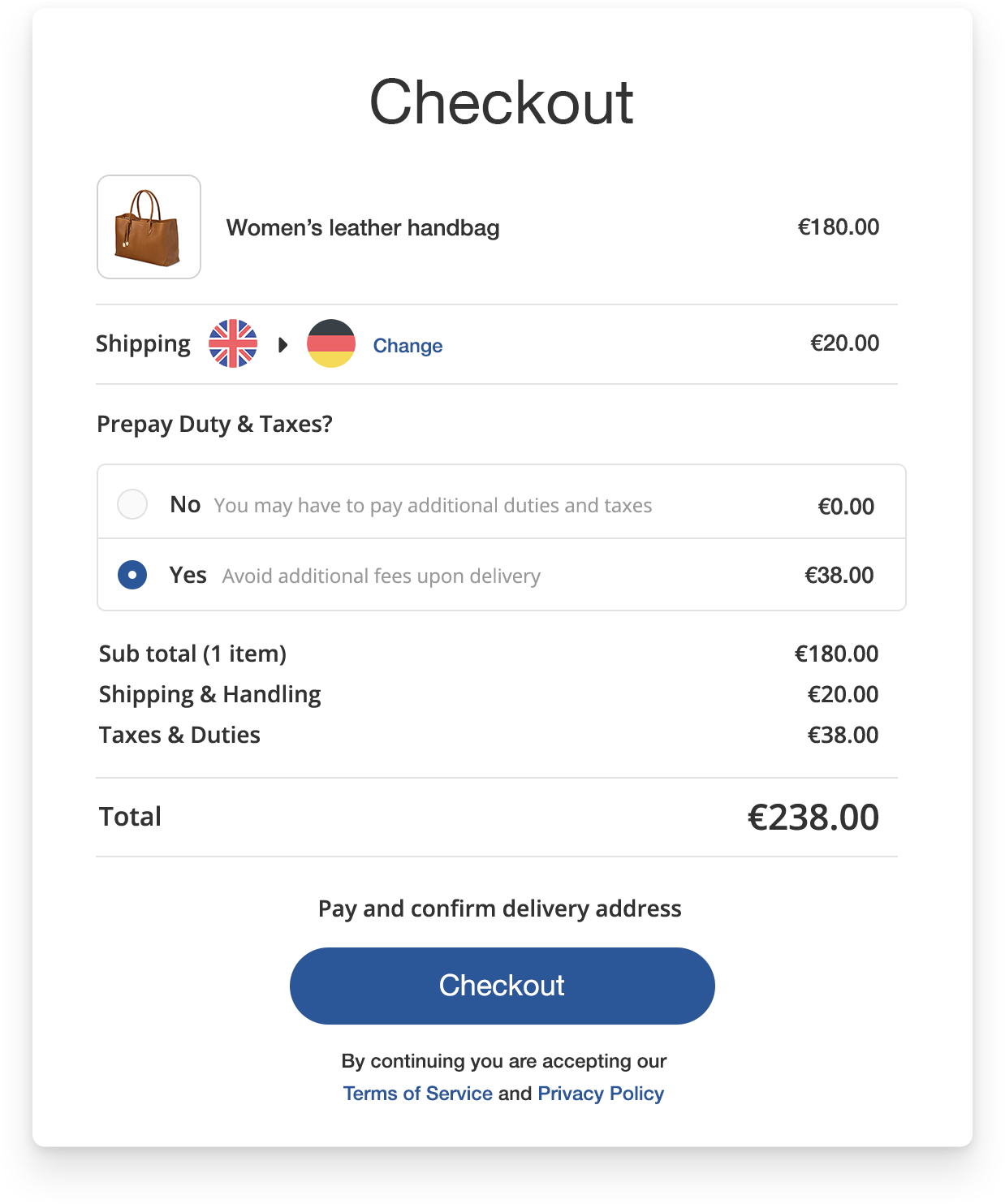

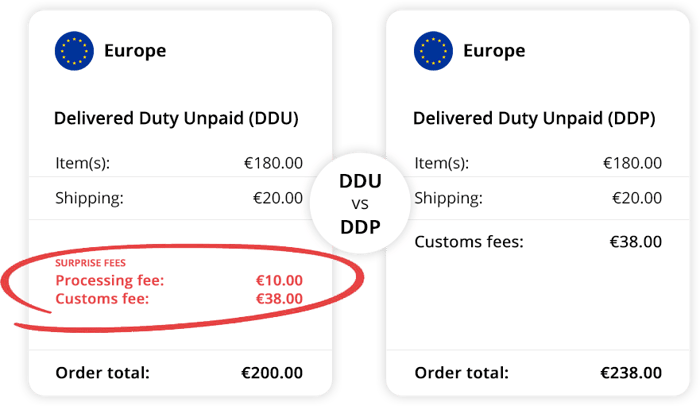

For countries outside of Europe, all orders over €150 are subject to customs tax and duties when entering Europe.

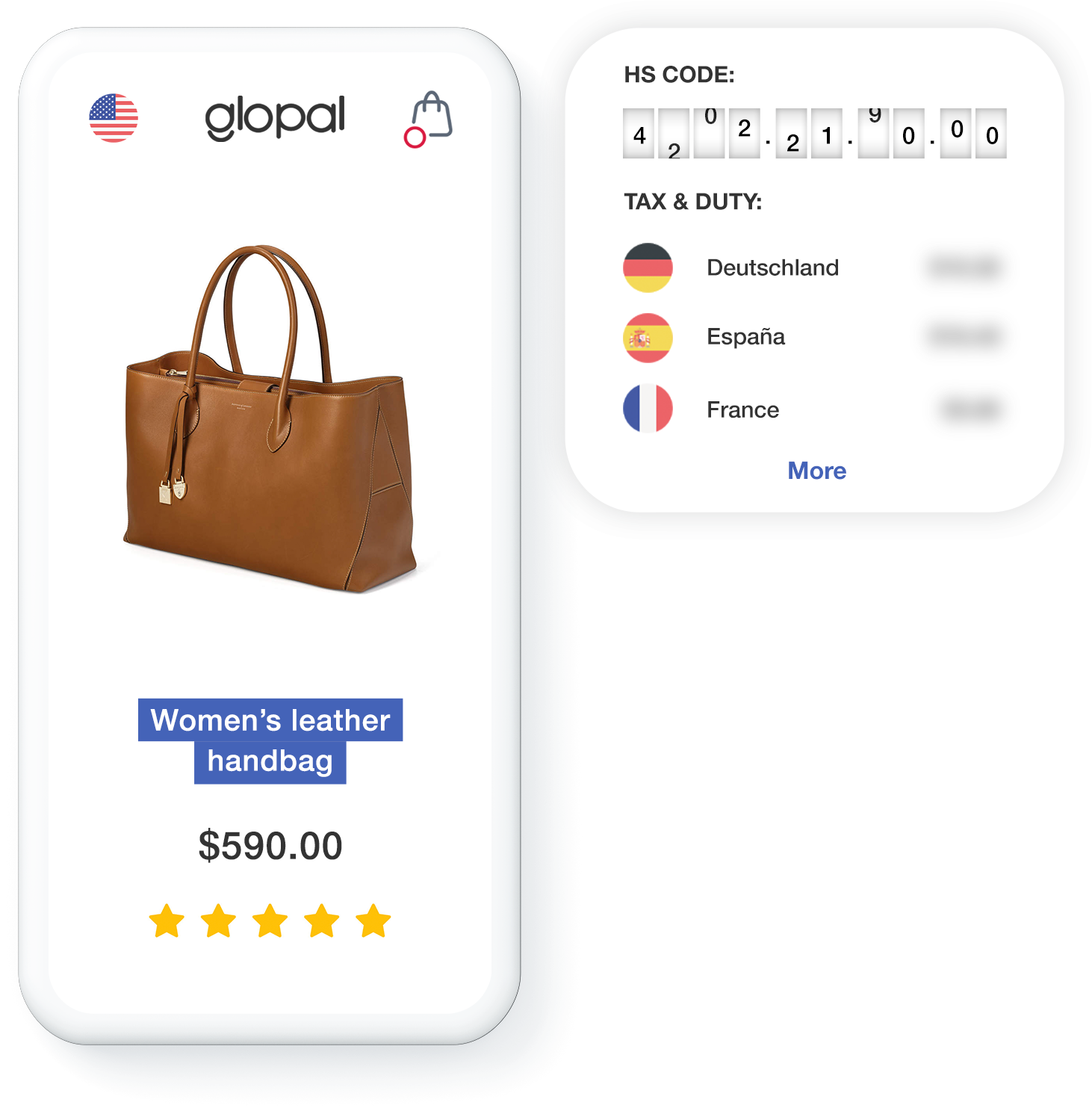

In order calculate the tax and duties for a given item, the item must be classified under the Harmonized System (HS).

The country of origin refers to the country of manufacture, production, or growth where a product or article comes from. Simply shipping a product through another country does not change the origin.

When importing items into Europe the item's country of origin is important. Depending upon the item’s country of origin different levels of tariffs may be applied.

Items with a British Country of Origin, for example, are not subject to customs duty when being imported into Europe.

Harmonized System (HS) code classification

The Harmonized System is an internationally standardized system of names and numbers to classify traded products. It came into effect in 1988 and has since been developed and maintained by the World Customs Organization (WCO).

In order to accurately calculate the customs Tax & Duty that needs to be applied to an item, the item must first be correctly classified under the Harmonized System (HS) with an HS Code. This can be done manually on a per item basis, but for the majority of merchants a manual approach is rarely a viable option. Instead most merchants will opt for automatic HS classification.

Customs clearance is the act of taking goods through the customs authority to facilitate the movement of cargo into a country (import) and outside the country (export).

All items being shipped to Europe from outside the European single market will need to go through customs clearance. If you don’t have the appropriate paperwork and approach this will cause delays to you and your customers.

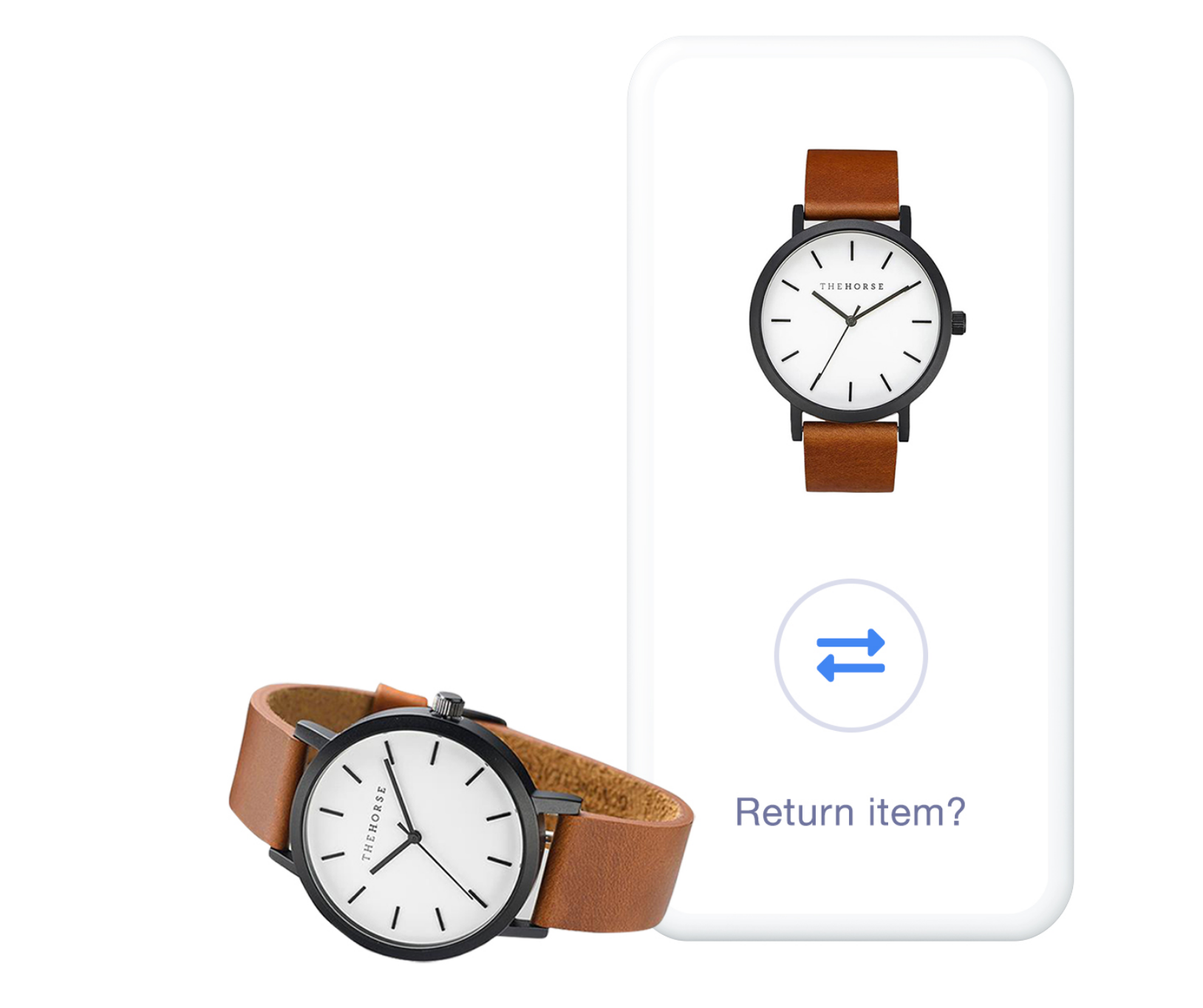

International transactions don’t end when a customer receives their order. European buyers must be provided with a compliant and easy to use returns process. Glopal's global returns solution ensures a streamlined system that is both easy for customers to navigate and affordable for merchants to manage.

Things to consider:

Recommendations: